PLTR Q3 2025 forecast

- Forecast: Wall Street analysts expect Palantir to post a quarterly revenue of approximately $1.09 billion.

- Historical context: This would mark a significant year-over-year increase, following strong growth in the second quarter where revenue surpassed $1 billion for the first time.

- Forecast: The consensus EPS forecast is around $0.17 per share.

- Historical context: This would represent a substantial year-over-year increase, continuing a trend of beating earnings estimates, which has been the case for several quarters.

- AI platform (AIP): Palantir’s artificial intelligence platform is a key growth catalyst. Its strong adoption, particularly in the U.S. commercial sector, has been noted by analysts as a primary driver of revenue growth.

- Government contracts: While the commercial sector is growing, government contracts remain a significant portion of Palantir’s revenue. Any instability, such as a U.S. government shutdown, could pose a risk to government revenue growth.

- International weakness: Some analysts have highlighted a lagging international commercial business, which could present challenges to global expansion and growth.

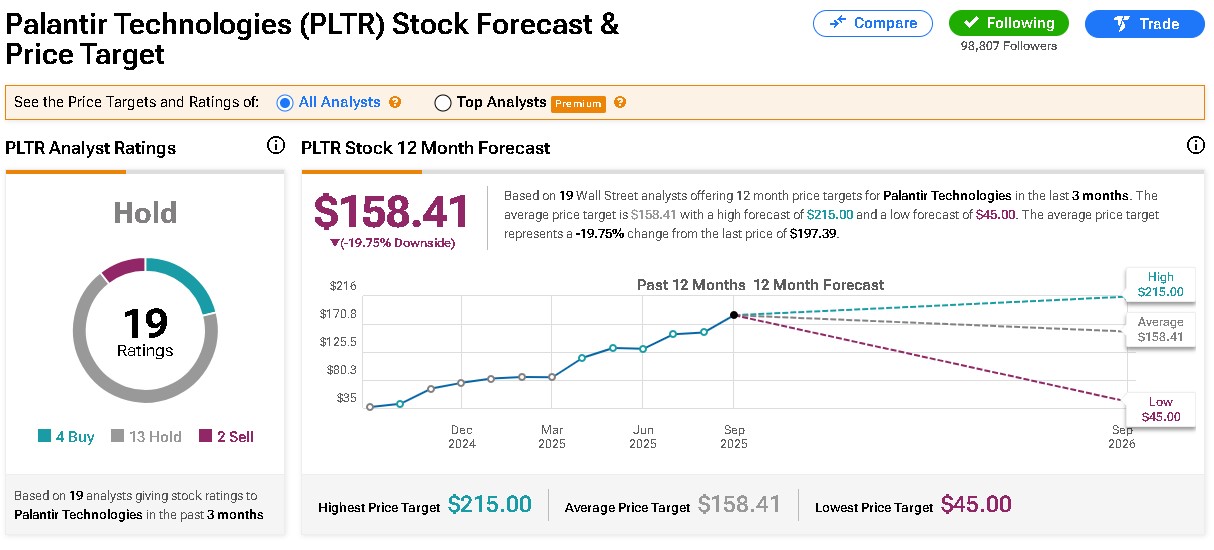

- Consensus: The average consensus rating for Palantir is “Hold”.

- Average price target: The average 12-month price target from multiple analyst firms is in the range of $162 to $198. This indicates that many analysts believe the stock is overvalued at its current price.

- Wide range: Forecasts vary widely, with a 12-month high target of $225 and a low target of $145.

- High valuation: Palantir’s valuation metrics, such as its Price-to-Earnings (P/E) ratio, are significantly higher than those of typical software companies, which introduces a greater risk of volatility.

- No room for error: With such rich valuations, a miss on key financial metrics or any guidance that questions the company’s growth could lead to a sharp decline in the stock price.

- Focus areas: Investors will closely monitor details on commercial AIP momentum, customer count, international revenue diversification, and any impacts from a government shutdown.

Palantir Could Put Investor Concerns to Rest on November 3

Palantir Technologies (NYSE: PLTR) is set to release its third-quarter earnings on November 3, 2025, and expectations are running high. Historically, Palantir’s earnings reports have acted as major catalysts for its stock. For example, when the company reported its strong Q2 results in August, shares surged sharply — mirroring similar reactions seen earlier in the year after back-to-back upbeat reports.

That consistent performance explains why Palantir shares remain up over 130% in 2025, despite recent volatility. With momentum building and prior concerns from the U.S. Army now resolved, investors may once again see the stock rally following its upcoming results.

AI Demand and New Contracts Strengthen the Outlook

Recent developments continue to highlight robust demand for Palantir’s AI software platforms. The company is expanding partnerships with existing clients while securing new, high-value contracts. A standout example is Palantir’s new partnership with the U.K. government, which could lead to as much as $1.8 billion in defense sector investment — potentially opening doors to one of Europe’s most lucrative markets.

These wins underscore why Palantir has consistently beaten Wall Street expectations for four consecutive quarters. In Q2, the company reported $1 billion in revenue, a 48% year-over-year increase, alongside $2.3 billion in newly signed contracts. That pushed Palantir’s total backlog to $7.1 billion, up 65% from the prior year — showing that its revenue pipeline is growing even faster than actual sales.

Strong contract growth has translated into impressive profitability. Adjusted earnings jumped 77% year-over-year to $0.16 per share, and operating margins climbed to 45% in the first half of 2025 — a nine-point improvement from the prior year. This steady margin expansion signals that Palantir still has room to scale profitably in the long term.

Valuation Remains High — But the Growth Story Justifies It

Despite its remarkable run, Palantir continues to face scrutiny for its lofty valuation, trading at a forward P/E ratio above 200. However, that premium reflects investors’ confidence in the company’s consistent execution, accelerating earnings growth, and expanding revenue backlog.

If Palantir delivers another strong quarter on November 3, it could reinforce its reputation as a leading force in the AI software and data analytics space — a market projected to grow exponentially over the next decade.

Despite recent market pullbacks, Palantir Technologies (NYSE: PLTR) remains one of 2025’s standout performers — up an impressive 137% year to date. That resilience reflects investors’ confidence in the company’s long-term vision and its ability to quickly address short-term concerns. Notably, Palantir confirmed that the issues previously raised by the U.S. Army were promptly identified and resolved, restoring confidence in its government business.

Looking ahead, demand for Palantir’s AI-driven software platforms continues to look exceptionally strong. Existing customers are deepening their partnerships, while new contracts continue to roll in across both government and commercial sectors. One key highlight is Palantir’s recent partnership with the U.K. government, involving potential investments of up to $1.8 billion in defense technology — a move that could further expand the company’s footprint in a highly lucrative international market.

These strategic wins are likely to support another earnings beat when the company reports Q3 results on November 3, 2025. Palantir has already exceeded Wall Street expectations for four consecutive quarters, driven by higher spending from existing clients and a growing roster of new customers. The steady inflow of new deals has also helped accelerate the company’s revenue pipeline, which has been expanding at a faster pace than realized revenue — a positive sign that Palantir’s growth trajectory remains intact.

Financial performance has mirrored that momentum. In Q2, Palantir’s adjusted earnings surged 77% year-over-year to $0.16 per share, while operating margins rose to 45%, marking a nine-point improvement compared to the same period last year. These metrics highlight the company’s increasing operational efficiency and scalability as demand for its AI solutions grows.

Even with this impressive performance, there’s still room for margin expansion and long-term profitability gains. If Palantir continues executing at its current pace, it appears well-positioned to maintain robust earnings growth throughout the coming quarters and sustain its leadership in the fast-growing AI software and data analytics market.

The Bottom Line

While valuation concerns persist, Palantir’s growth trajectory remains compelling. The company continues to strengthen its position in both government and commercial sectors, building a diversified and durable revenue stream.

For long-term investors, it makes sense to hold onto Palantir shares, as another strong earnings report could help the stock regain momentum — and potentially set the stage for continued growth well into 2026 and beyond. We believe estimated price range post-earnings: $189–$240, with $210 as a balanced, realistic expectation under optimistic conditions.